Singapore's approach to sustainability reporting has shifted decisively. What was once encouraged is now required, and the requirements are getting stricter each year. Whether you're a listed company on the SGX, one of Singapore's largest private businesses, or a supplier to any of the above, the question is no longer whether climate reporting applies to you. It's how prepared you are.

This guide breaks down Singapore's current climate reporting framework, who it applies to, what the key deadlines are, and what your business should be doing right now to stay ahead of them.

Singapore's climate reporting framework at a glance

Singapore's mandatory climate reporting regime is built around the ISSB (International Sustainability Standards Board) standards, specifically IFRS S1 and IFRS S2. It was developed jointly by the Accounting and Corporate Regulatory Authority (ACRA) and SGX RegCo, and it follows a phased approach that rolls out requirements based on company size and listing status.

The framework covers three types of disclosures:

- Scope 1 and Scope 2 GHG emissions: direct emissions from operations and indirect emissions from purchased energy

- Scope 3 GHG emissions: indirect emissions across the full value chain, including suppliers, logistics, and product end-of-life

- Full ISSB-based Climate-Related Disclosures (CRD): broader disclosures covering governance, strategy, risk management, and climate-related targets

Timelines are tiered by company type. In August 2025, ACRA and SGX RegCo extended several deadlines to give companies more time to build the necessary capabilities, but the direction of travel remains firmly towards greater disclosure and higher scrutiny.

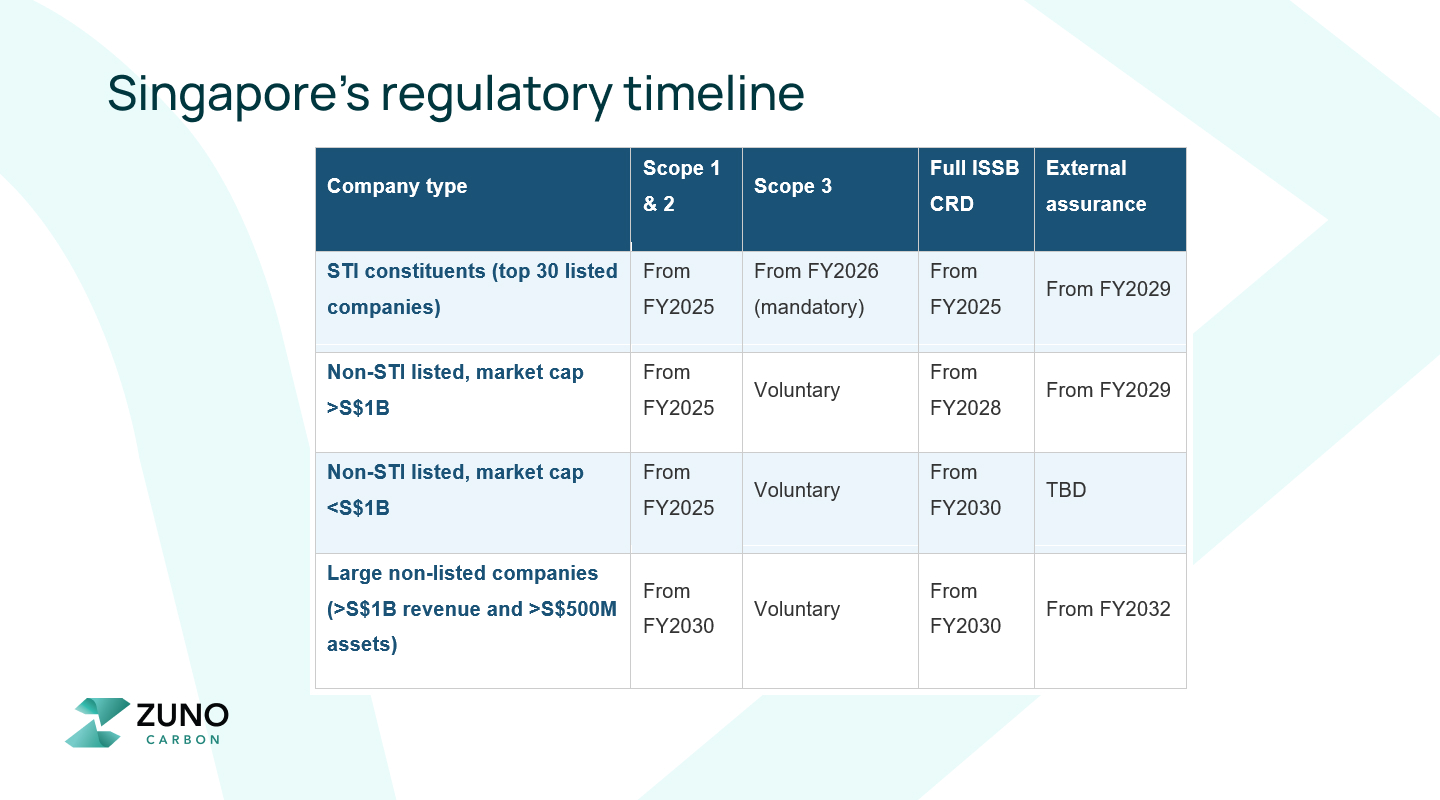

The regulatory timeline: who needs to do what and when

Here is a full breakdown of the current reporting requirements across all company categories:

Spotlight: SGX listed companies

If your company is listed on the Singapore Exchange, mandatory climate reporting is already here. From FY2025, all SGX-listed companies must disclose Scope 1 and Scope 2 GHG emissions as part of their annual reporting cycle, regardless of market capitalisation or size.

For many companies, this is the first time emissions data has had to be formally measured, verified, and disclosed to investors and regulators. The most common challenges at this stage include:

- Data gaps: energy and emissions data is often scattered across multiple systems, sites, and business units with no single source of truth

- Inconsistent methodologies: without a structured framework, different parts of the organisation may be calculating emissions using different approaches, making consolidation unreliable

- Audit readiness: external limited assurance on Scope 1 and 2 data becomes mandatory for all listed companies from FY2029, meaning the data collection processes put in place now need to be defensible in the future

For non-STI listed companies with a market capitalisation above S$1 billion, the next major milestone is full ISSB-based climate-related disclosures from FY2028, covering governance, strategy, risk management, and climate targets. That may feel distant, but building the data infrastructure to support those disclosures takes time, and the companies that start now will be in a significantly stronger position than those that wait.

Spotlight: STI constituents and the Scope 3 moment

The Straits Times Index represents Singapore's 30 largest listed companies by market capitalisation, including names like DBS, Singtel, CapitaLand, and Keppel. For these companies, 2026 marks a significant step up in reporting obligations: Scope 3 GHG emissions are now mandatory from FY2026, making Singapore's top 30 the first companies in the country required by law to measure and disclose their full value chain emissions.

This is a meaningful threshold. Scope 3 emissions typically represent 70 to 90 percent of a company's total carbon footprint and are significantly harder to measure than Scope 1 and 2. They require data from suppliers, logistics partners, customers, and contractors, which means that collecting them is as much a relationship and process challenge as it is a technical one.

STI companies that are still in early stages of building their Scope 3 programmes face several immediate challenges:

- Supplier data collection: getting reliable emissions data from dozens or hundreds of suppliers requires structured engagement programmes, standardised templates, and persistent follow-up

- Estimation and methodology: where primary supplier data is unavailable, companies must use spend-based or industry average estimates, each with their own limitations and disclosure requirements

- Category prioritisation: the GHG Protocol defines 15 categories of Scope 3 emissions. Not all are equally material for every company, and identifying which categories to prioritise is itself a significant piece of work

- Audit readiness: Scope 3 data will eventually need to withstand external scrutiny, which means the collection and calculation processes need to be documented and defensible from day one

FY2026 is already underway, which means STI companies need to be collecting Scope 3 data now, not planning to start. For companies that are still in the early stages, the window to get this right before reporting deadlines is narrowing quickly.

The ripple effect: what this means if you are not listed

Even if your company is not listed on the SGX, Singapore's climate reporting framework is likely to affect you sooner than the official timelines suggest. Here is why.

When STI companies are required to report Scope 3 emissions, they need data from their suppliers, partners, and service providers. That pressure flows down the supply chain to companies of all sizes, including private businesses that are not directly subject to any disclosure mandate. If you supply goods or services to a listed company in Singapore, you may already be receiving requests for emissions data, and those requests are going to become more frequent and more specific as reporting requirements tighten.

For large non-listed companies, the formal requirements begin in FY2030, but the companies that start building their measurement capabilities early will be better positioned to respond to customer demands, support due diligence processes, and avoid being de-selected from supply chains that increasingly require verified sustainability data.

What your business should be doing now

Regardless of where your company sits in the reporting tiers, there are practical steps that apply across the board:

- Understand your tier and timeline. Start by confirming which category your company falls into and what the specific reporting requirements and deadlines are for that tier.

- Get Scope 1 and 2 right first. For all listed companies, these are already mandatory. If your data collection for Scope 1 and 2 is still fragmented or inconsistent, fixing that is the most urgent priority.

- Start Scope 3 planning now. For STI companies, FY2026 is already live. For others, voluntary early adoption gives you a head start on what will eventually become mandatory, and sends a clear signal to investors and customers.

- Build for auditability from the start. External assurance requirements are coming for all listed companies from FY2029. The data processes and governance structures you put in place now will determine how ready you are when that moment arrives.

- Invest in the right tools. Spreadsheets and manual data collection are not built to handle the volume, accuracy, and traceability that climate reporting now demands. Platforms that centralise data collection, automate validation, and maintain a full audit trail make the reporting process significantly more manageable.

The window to prepare is open, but not indefinitely

Singapore's phased approach to climate reporting was designed to give companies time to build capability, not to delay indefinitely. The timelines have already been extended once. The direction of travel is clear, and the expectations of investors, regulators, and business partners are only going in one direction.

The companies that treat this as a compliance checkbox will find reporting season increasingly painful. The ones that invest in building proper data infrastructure now will find it becomes a genuine advantage, both in terms of operational insight and in how they're perceived by the market.

If you'd like to understand how Zuno Carbon can help your team meet Singapore's climate reporting requirements, book a demo with us today and we'll walk you through it.

FAQs

1. What is the difference between SGX listed companies and STI constituents?

SGX listed companies are any of the 600+ companies listed on the Singapore Exchange. STI constituents are the top 30 of those companies by market capitalisation, essentially Singapore's largest and most prominent publicly listed businesses. STI companies face earlier and more stringent reporting requirements, including mandatory Scope 3 disclosure from FY2026.

2. Is Scope 3 reporting mandatory for all Singapore companies?

No. Scope 3 reporting is currently mandatory only for STI constituents from FY2026. For all other listed and non-listed companies, Scope 3 disclosure remains voluntary for now. However, the supply chain pressures created by STI companies needing Scope 3 data from their suppliers mean that many companies will face de facto requirements even without a formal mandate.

3. What are IFRS S1 and IFRS S2?

IFRS S1 and S2 are international sustainability reporting standards issued by the International Sustainability Standards Board (ISSB). S1 covers general requirements for sustainability-related financial disclosures, while S2 focuses specifically on climate-related disclosures including governance, strategy, risk management, and GHG emissions. Singapore's mandatory reporting regime is built around these standards.

.webp)